Rs 2,384 Crore

GST Fraud Racket Exposed in Bengaluru

Karnataka’s largest fake Input Tax Credit scam unravels 127 shell companies. How businesses can protect themselves from tax evasion networks and compliance risks.

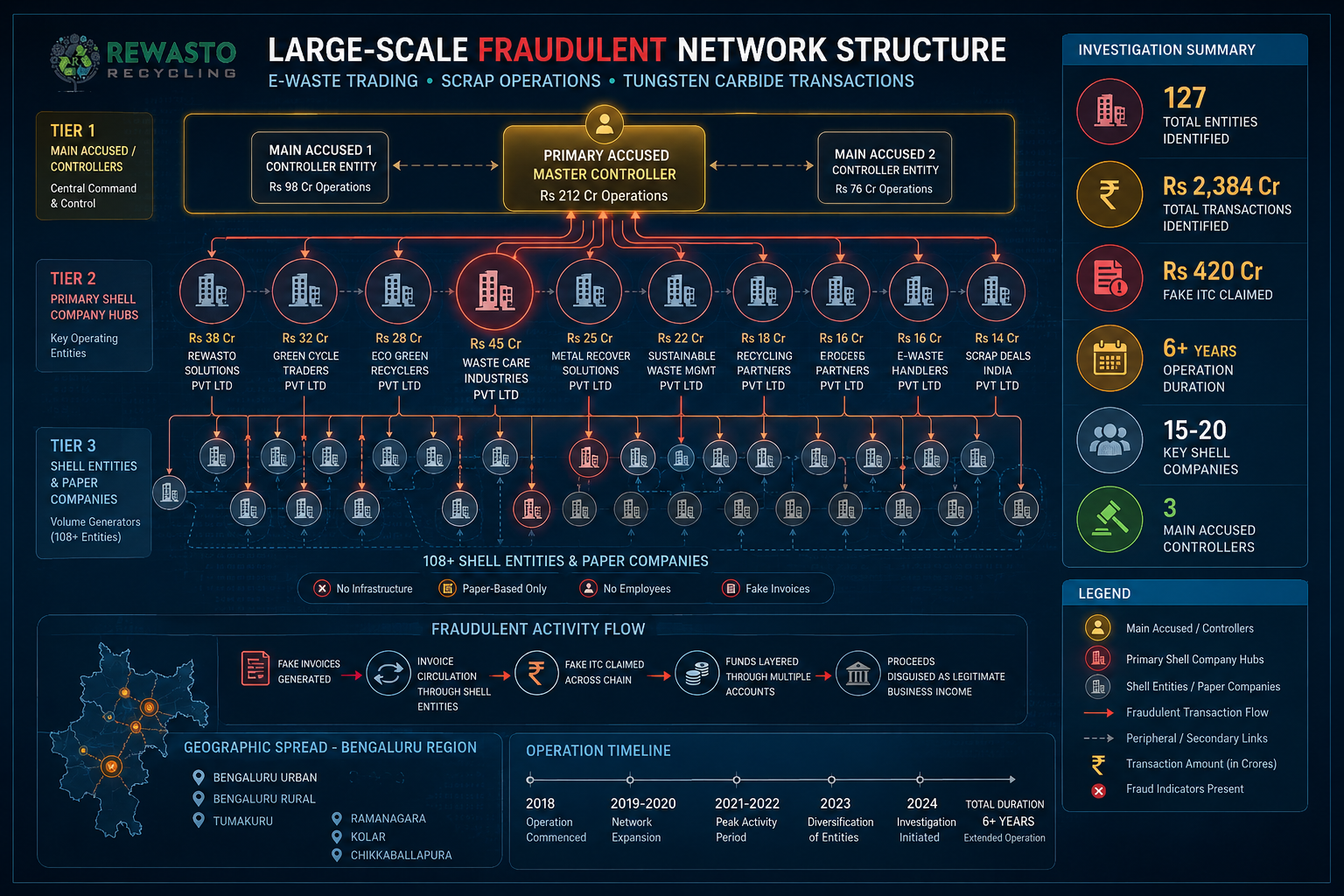

In one of the largest GST fraud operations uncovered in recent years, the Karnataka State Commercial Taxes Department has dismantled a sophisticated fake Input Tax Credit (ITC) network operating across Bengaluru and surrounding regions. The investigation revealed fraudulent transactions worth Rs 2,384 crore spread across 127 shell companies, with fake ITC claims totaling Rs 420 crore.

Two key accused have been arrested: one associated with K.H. E-Waste Recycler in Nayandahalli, who allegedly operated 55 fake supplier firms generating Rs 212 crore in suspicious transactions and Rs 38 crore in fraudulent ITC claims. The crackdown was executed jointly by the Enforcement Wing (South Zone) and the Service Analysis and Intelligence Wing of the Commercial Tax Department, demonstrating increasing coordination between state and central authorities.

⚠️ Investigation Finding

The network had been operating for an extended period using fabricated documentation, manipulated invoices, and shell business structures designed specifically to evade tax detection systems.

Investigation data reveals complex shell company network with artificially inflated turnover and zero actual business operations.

How The Scam Operated

The operation demonstrates sophisticated understanding of GST infrastructure vulnerabilities. Here’s how the fraudsters operated:

🏢

Shell Entity Creation

Multiple paper-based firms with no warehouses, employees, transport records, or actual business infrastructure.

📄

Fake Invoicing

Manipulated invoices and fabricated documentation designed to pass initial portal verification checks.

🎯

ITC Claims

Fraudulent Input Tax Credit claims without corresponding actual goods or services supplied.

📈

Turnover Inflation

Companies showing abnormal rises in turnover despite zero physical business activity or operations.

📌 Modus Operandi

The scam specifically targeted the e-waste and scrap trading sectors, leveraging regulatory complexity and lower scrutiny levels in these industries compared to mainstream manufacturing.

Red Flags Every Business Should Know

Investigators identified several warning patterns that regulatory bodies now prioritize during compliance audits. Companies should conduct self-audits against these markers:

Red Flag

What It Indicates

Risk Level

Suppliers with no physical presence or infrastructure

Potential shell company network

Critical

Abnormal turnover spikes without corresponding business growth

Fabricated sales documentation

Critical

No transport, warehouse, or employee records

Paper-based operations only

Critical

Invoices from suppliers in low-regulation sectors

Easier to create fake billing chains

High

Circular trading patterns or repetitive invoice cycles

Artificial transaction generation

High

Supplier GST IDs with mismatched PAN or address records

Identity manipulation or shell registration

High

Effective supplier due diligence and invoice verification are critical to avoiding inadvertent participation in fraud networks.

Business Impact and Liability

Companies must understand that even unintentional involvement in fraudulent ITC networks carries severe consequences. The liability does not fall solely on the fraudster but extends to all parties in the transaction chain.

A company that unknowingly accepts fake invoices from suppliers can face disallowance of ITC claims, penalties, and even potential criminal prosecution if authorities determine negligence in supplier vetting.

Enforcement Intensification: What Changed

This case represents a broader shift in GST compliance enforcement. The government is now employing:

Cross-referencing GST portal data against GST filings: Automated detection of mismatches between declared suppliers and actual transactions

Real-time GSTR monitoring: Continuous tracking of GST returns for suspicious filing patterns and supplier networks

Multi-agency collaboration: Joint operations between state commercial tax departments, CBIC, and ED for integrated enforcement

⚠️ New Reality

Authorities now treat supplier due diligence failure as negligent compliance, increasing corporate liability even when fraud is initiated by suppliers rather than the buyer company.

How to Protect Your Business

1. Implement Robust Supplier Verification

Before onboarding any supplier, verify GST registration, physical business location, and business continuity records. Cross-check GST NTIN with MCA records and DGFT databases. Document all verification activities.

2. Monitor Invoice Authenticity

Establish an internal protocol to validate invoices against supplier registration details, declared business activities, and historical transaction patterns. Flag invoices from sectors with higher fraud prevalence (e-waste, scrap, recycling).

3. Maintain Detailed Records

Retain all supporting documents for supplier interactions, verification activities, and invoice authenticity checks. This documentation becomes critical if authorities question your ITC claims.

4. Conduct Periodic Internal Audits

Hire external auditors to evaluate your GST compliance posture quarterly. Identify and eliminate suppliers exhibiting red flags before regulatory action occurs.

5. Track GST Notifications and Circulars

CBIC regularly issues alerts on fraudulent seller networks and high-risk invoice patterns. Subscribe to official CBIC communications and adjust procurement practices accordingly.